.webp)

Dear community,

I'm addressing you from a plane again while listening to Xavier Rudd, again. I'm flying back from my hometown Porto, after a week there with my kids, both my parents, and my two sisters - a rare coincidence considering we live in four different cities across three different countries. I hope you get to see a lot of family and friends this Summer too.

Lately I've been thinking a lot about Goparity’s “why” and the importance of every company having one and communicating it all the time. It is an obvious concept, popularized years ago in a TED talk by Simon Sinek, but something we don’t always keep in mind.

Our “why” is clear: we exist to foster the transition to a more sustainable economy by providing access to capital to companies and projects that want to do things well, while giving their investors a return that goes well beyond the positive impact the projects generate.

In doing so, we’re also empowering people to choose where their money goes and giving them the satisfaction of knowing it is being used for good.

📢 Our “why” is now more relevant than ever: the “Banking on Climate Chaos” report

The 2024 “Banking on Climate Chaos” report just came out and makes it clear that our “why” is now more relevant than ever. I’ll only share a few highlights but their website is worth browsing and the report is worth dedicating some time to.

😱 The world’s biggest 65 banks have dedicated $7,9T to fossil fuel financing in the past 9 years (since the Paris Agreement). Yes, $7.900.000.000.000.

📊 2/3 of them increased their commitment to fossil fuel financing in 2024. Only two out of the top 30 didn’t.

🛢️ Overall investment grew by 23% from 2023 to 2024.

🎖️ JP Morgan Chase (#1) and other US major banks are the undisputable leaders, while Canada (Royal Bank of Canada #8, Toronto-Dominion #9) and Japan place two banks each on the Top10.

🇬🇧 UK’s Barclays is the only European Bank in the Top 10, while HSBC ranks #20.

🇪🇸🇫🇷🇩🇪 Other European “leaders” are Santander (#18, ES), Deutsche Bank (#23, DE), BNP Paribas (#24, FR) and Credit Agricole (#27, FR).

🙏 On the bright side, quite a few European banks have reduced their investment: La Caixa (#49, ES) and ING (#32, NL) performed the most significant reductions.

🎆 Highlights of Q2 2025

The last quarter, as usual, had its ups and downs

🚀 We reached 50M€ invested via Goparity.

🤝 We closed a 2.9M€ funding round late in April, led by 3XP, with the participation from Mustard Seed Maze, Schneider Electric, Regenerative.eco, InvestEco and more than 800 small shareholders, many of which are Goparity users, via Crowdcube.

🧑It was great to see all the team get together in Lisbon in our shareholders' MAZE offices (picture below).

🔃 You can now instantly transfer funds within your Goparity wallets. For free. This means more flexibility and faster access to investment opportunities - no more money stalled.

⚡️ We raised 500k€ for Dispower, providing +3000 families with access to electricity.

👩 We held our first board meeting in gender parity: 3 women and 3 men. This also is walking the talk.

🇪🇺🇨🇦 We concluded our B-Corp re-certification, which also included Goparity Canada for the first time: our score increased from 84.3 points to 93.2 🌱🙌

🌾News about our ongoing loans

🌱Jord (🇩🇴 🇸🇪) was nominated for the 2025 Earthshot Prize by the Caribbean Climate-Smart Accelerator and has become a member of both the World Bioenergy Association and Bioenergy Europe.

👷🏻Efenco (🇪🇪) was successfully implemented. The funds were used for the research and development, piloting and testing of their HERC technology, which has brought the system closer to commercial readiness.

☀️ Solar Sustainable Aquaculture, Solar Herdade do Baldio and Solar Bakery (🇵🇹) have been successfully implemented, ie solar panels are installed and producing clean energy.

🍇 Fita preta (🇵🇹) won the “Best Wine Tourism in Portugal” award of by the Portuguese Wine Tourism Association (Associação Portuguesa de Enoturismo).

🏫 Goparity Canada (🇨🇦) funded Solar fo Gw’sala - 'Nakwazda'xw in record time: a rooftop solar system in a First Nation School’s gym in British Columbia.

In the past quarter we recovered 24 payments in arrears from 11 projects, had 2 loans restructured and prevented 22 payments from being delayed via early detection warnings implemented by our Operations team.

Our NPL > 90 days at the end of 2024 was 7,56% lowering from 14,95% observed at the end of 2023. Still, we are very focused on improving these numbers, continuously employing efforts to optimize our credit policy and recovery procedures. Check the recently published 2024 Default Rate Report >

Regarding project updates, as per our commitment, we have zero projects in arrears with updates older than 180 days.

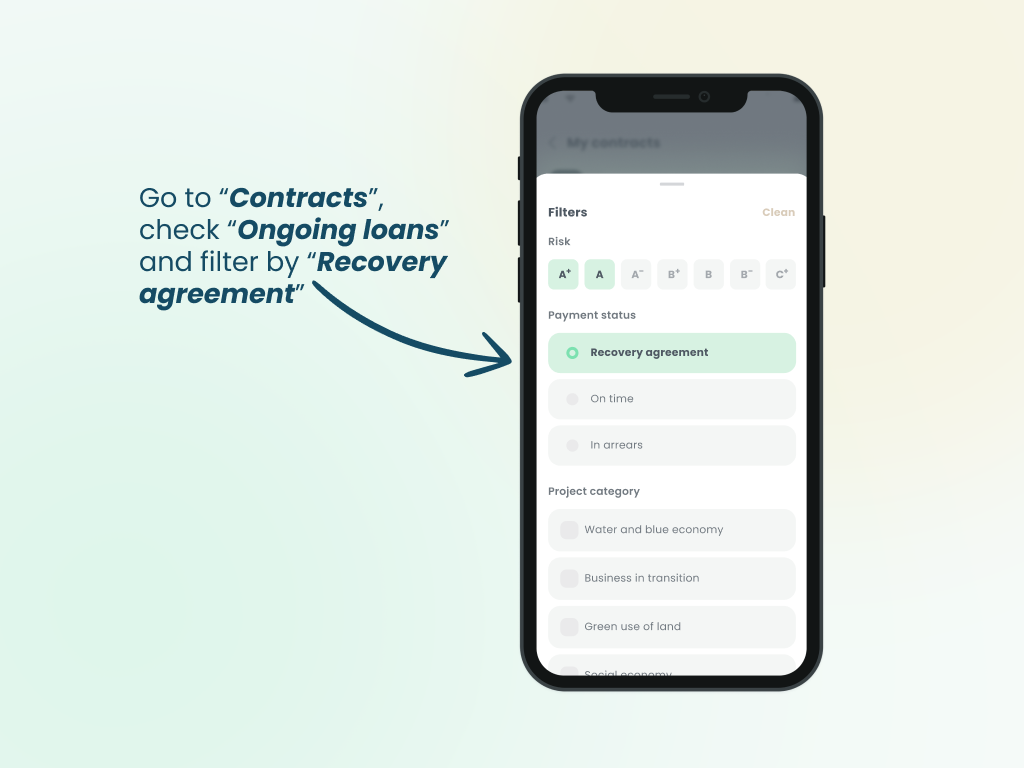

🆕 Credit recovery and new info on your dashboard

I know it’s not always as visible or successful as we’d like, but we put tremendous effort into credit recovery, and are already seeing positive results.

Until recently, your dashboard would show a project as “in arrears” even if a judicial or extra-judicial recovery plan had already been agreed upon and the promoter was actively complying with it.

Now, when you access your ongoing loans in your dashboard, you will see the new category, "Recovery agreement”. This allows you to easily identify which projects are no longer in arrears and the borrower is successfully following the recovery payment plan.

🛡️ New commitments regarding risk: asset-backed loans

Last quarter we had to endure the insolvency of two companies that received financing from Goparity a few years ago. Unlike most other cases - where we were able to recover debt, agree on new payment plans or restructure loans - there was no recovery of funds. This happened, in big part, because we had no pledge on assets or guarantees.

When we take a pledge on assets, be it buildings, machinery, solar panels, or even receivables it provides us with "secured" credit status. This means our debt becomes senior to others (up to the amount of the collateral/security provided) which is beneficial not only in case of insolvency, but also in other judicial credit recovery procedures.

👉 Having a guarantee does not affect a loan’s risk rating. The risk rating measures of how likely the company is to be able to perform its loan obligations, while guarantees are only activated in case of default - but it does impact the interest rate of a given loan. If a pledge is properly registered the risk of loss of all capital is near-zero.

How we measure a project's risk > What are guarantees for >

Our commitments moving forward 👇

- Prioritizing projects that offer guarantees: from corporate guarantees to pledge of buildings, land, equipment or receivables.

- Make it clearly visible when a project does (or doesn’t) offer a guarantee or collateral (even on our social media posts - check below)

- Communicating the Loan-to-Value (LTV) ratio of collateralized projects: this means we’ll let you know how much the lent amount is worth in comparison to the value of pledged asset (e.g.: a 70.000€ loan backed by an asset that is worth 100.000€ has a 70% LTV)

For a long time now, you can check whether a loan has a guarantee or not in the campaign page (image on the left). That information is also available in the Key Investment Information Sheet.

We're now also publishing that information whenever we share a new investment opportunity on Instagram or LinkedIn. On the image on the right you can see the example of what that looked like for Bioo: powered by nature.

🙋♂️The question

We often reject really impactful projects, because we cannot be sure about their capability to generate income to cover the debt they'de raise and they own no assets to provide as collateral.

Some examples could be startups, either technological or not, or early stage or projects in sectors like health, education or social impact.

Still, we believe people can play a role in providing them with access to finance and deserve a significant upside should they become successful businesses in the future.

My question this time is: would you be available to invest in equity - becoming a shareholder - in impactful companies?

(Click in one of the options below to answer 👇)

This would not imply any obligation as a shareholder (we’d do the job for you), but it means the potential gains could only come from:

- A secondary sale of your shares (selling to another investor in the future);

- The company becoming profitable and pays dividends;

- The company being acquired;

- The company being listed on the stock market.

Yes, absolutely

I don't think so

👋 What to expect from this semester

I believe I already told you about how I only like to talk about things when they’re 99% confirmed (better if 100%). I don’t like to create to many expectations ahead of time, even less, to come out as inconsequent. It is happening with ETF investing for example, where the formal regulatory approval is taking much longer than expected. But the plan is still there and evolving, I assure you.

🇪🇸🇪🇺 Bioo is currently online with the most innovative technology we ever funded: generating electricity from the soil. They have installations from Spain to the Middle East;

🇵🇹🇪🇺 Sea4us came back to Goparity: after the early settlement of one of our biggest loans ever, they’re back with our largest campaign ever, they plan to raise up to 1,2M€ to reach clinical trials in 2026;

🇨🇦 Plaex, a company turning construction waste into building brick, is fundraising in Goparity (offer available to Canadian investors only);

🇨🇴 Colombian companies will be back to the platform with more exciting projects on the Agrifood and Energy sectors;

There’s actually another piece of exciting news that are very likely to be heading our way but I don’t want to talk ahead of time. Promise to follow-up on my next email 🙏

Thanks for getting to the end of this message, I know it was a long one and respect you for that. Have a great summer!

If you believe in what we’re building at Goparity, please share your experience. Your feedback not only helps us improve, but also helps more people discover impact investing.

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)